After the fun and excitement of the holidays, it’s common to start the year with a little buyer’s remorse. Perhaps you overspent on gifts, holiday décor, food, travel, or all of the above.

The good news though, is that it’s a new year, and you can start off on the right foot simply by planning a budget and trying your best to stick to it.

When it comes to allocating your money, there are many schools of thought. Consider your options and choose a plan that will work with your lifestyle.

First Things First – Why Are You Doing This?

It can be overwhelming to think about budgeting, especially when you’ve tried it before and not much changed as a result. The key is to make a plan that is realistic and sustainable.

Perhaps you’re having an internal battle – in your mind you know a budget is necessary, but in your heart, you’re daydreaming of an upcoming concert, weekly splurges on delicious dinners, or a well-deserved vacation.

The solution? Join your head and your heart by getting in touch with your inner desires and use that to motivate you to do better and actually stick with your plan. You’re less likely to cheat your own system if you look at the big picture and keep your eyes on the prize.

Ask yourself: What are my goals? What is my motivation for budgeting?

- Saving for vacation or retirement

- Paying off debt

- Buying a house

- Building an emergency fund

Once you determine your main motivator(s) for budgeting, make a few visual reminders to yourself so you can stay focused. You can do this by putting a sticky note or a picture in a few places you’ll come across frequently.

For example, if you’re saving for a house, you could put a picture of your dream home on your fridge, mirror, or phone’s lock screen to help remind you of your goals.

Crunch the Numbers

Before setting up a budget, you’ll first need to take a hard look at your monthly income as well as your expenses. Ask yourself the following questions:

- What is my total “take home” pay after taxes? Include the following:

- Wages

- Money from side gigs

- Alimony and/or child support

- Any other regular income you receive

- What are my current expenses?

- Rent or mortgage

- Utilities and internet bill

- Insurance (health, car, life, renter’s or homeowner’s, etc.)

- Average gas costs

- Debt (credit card, student loans, car payment, medical bills, etc.)

- Groceries

- Childcare

- Subscriptions (streaming services, gym memberships, etc.)

- Dining out

- Entertainment

- Clothing

- Gifts, travel, miscellaneous

- Annual fees*

- Seasonal expenses*

When looking at your income and expenses, think through every expenditure and classify each one as either a “want” or a “need”.

*Be sure to also include annual fees as well as seasonal expenses. For instance, there are things you may not see reflected in this last billing cycle – things that show up in other parts of the year, nonetheless. Perhaps July tends to be an expensive month for you, due to summer travel, birthdays, or otherwise. Be honest with yourself and round up when calculating your typical costs, otherwise your data will not reflect reality and therefore it will be harder to shift yourself into a sustainable budget plan.

Categorize Your Expenditures and Choose a Plan

There are many tried-and-true budgeting styles; you just need to find the one that works best for you. Most of these schools of thought revolve around the concept of initially categorizing your expenditures into two main categories: wants and needs.

From there, you can divide it up much more precisely, but it all starts with an initial assessment of essentials vs. non-essentials.

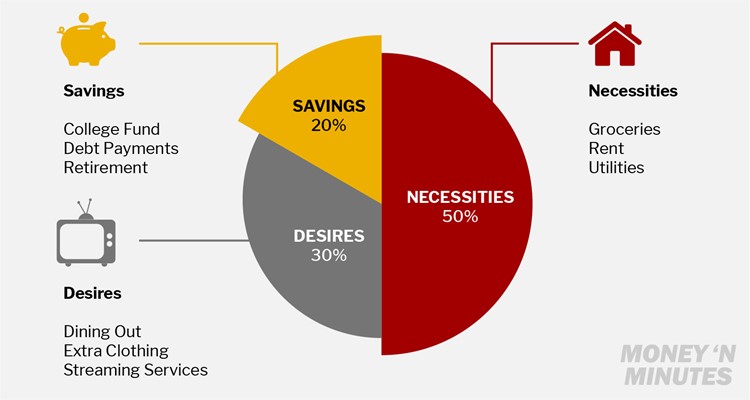

The 50-30-20 Rule

With the 50-30-20 rule, you plan to distribute your income into the following categories:

- 50%: Necessities

- 30%: Desires

- 20%: Savings and debt

Necessities include things like rent, groceries, and utilities, whereas desires would include dining out, movie tickets, new shoes, and Netflix. Sorry, but it’s true – Netflix binging is a “want”, not a “need”.

This means that if your monthly paycheck after taxes is $2,000, you have approximately this much money to allocate to each category:

- Necessities: $1,000

- Desires: $600

- Savings and debt: $400

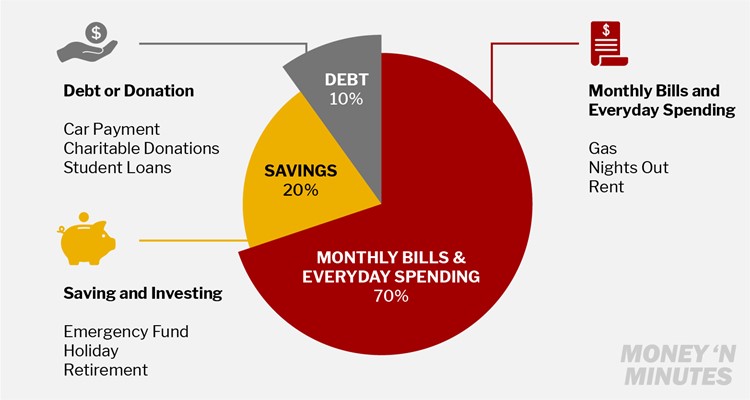

The 70-20-10 Rule

The 70-20-10 rule is a little different. With this system, your funds are divided up according to these categories:

- 70%: Monthly bills and everyday spending

- 20%: Saving and investing

- 10%: Debt or donation

A benefit to this method is that you don’t have to decide between “wants” and “needs” because it all goes into the same bucket. However, this could also make things more confusing, depending on how you look at it.

Therefore, with the same example of a monthly take home pay of $2,000, you’d have approximately the following amounts for each category:

- Monthly bills and everyday spending: $1,400

- Saving and Investing: $400

- Debt or donation: $200

Which Is Best for You?

As you can see in the examples above, the two rules are similar, but yield very different results. One key distinction is the way in which debt and savings are categorized.

The bottom line is, there is no one-size-fits-all answer when it comes to finding a budget style that best matches your specific lifestyle and priorities.

Run the numbers for both systems and see what would work best for you and your unique situation. Try it out for a month or two and revise as needed. Remember, you can also create subcategories within each larger grouping. Customize it to fit your needs!

Get Back on Your Feet

Think of the famous saying, “Shoot for the moon. Even if you miss, you’ll land among the stars.” This applies to budgeting, too.

If you set a budget for yourself and your efforts fall short, don’t be too hard on yourself. Chances are you still did better than you would’ve if you hadn’t made any sort of budget at all. Revise your plan and try again next month.

It takes time for big changes to settle in and become long-term habits. In the meantime, if you find yourself in need of some extra cash to get you through, Money ‘N Minutes of Kansas City has your back.